QIMA 2023 Q3 Barometer

Q3 2023 Barometer: ESG Legislation Progress Means No More Business as Usual in Supply Chain Sustainability

Halfway through 2023, much-awaited progress in European supply chain due diligence legislation is introducing an era where ESG (Environment, Social and Governance) compliance becomes mandatory, and the emphasis on closely examining suppliers keeps growing. Meanwhile, sourcing insights collected by QIMA show that even as Western buyers pursue greater supply chain diversification overseas and close to home, China remains ever-present in global procurement.

This barometer report, informed by QIMA’s consumer goods data on inspections and audits in addition to the findings from our H1 survey of 250+ businesses with international supply chains, offers a snapshot of how the global sourcing landscape is transforming in the wake of the seismic disruptions of the past few years.

ESG Performance Rises on Supply Chain Agendas Worldwide

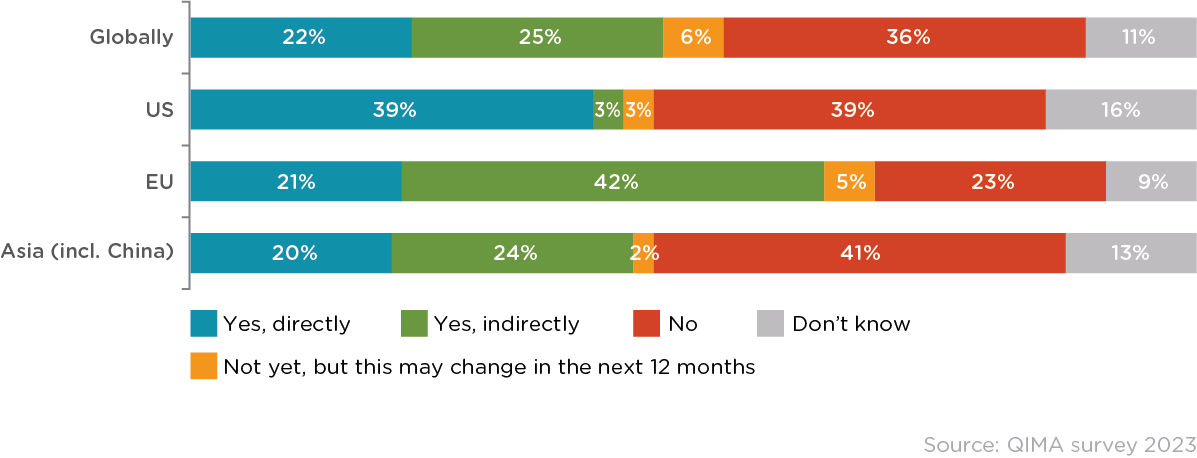

With Germany’s Supply Chain Act already in force, and the EU Directive on Corporate Sustainability Due Diligence (CSDDD) moving through the legislature, 2023 is seeing sustainability concerns rise rapidly through the agendas of businesses worldwide. QIMA’s H1 2023 survey shows that the increasing focus on ESG concerns is having a knock-on effect even outside of the immediate scope of relevant laws: almost half (46%) of respondents reported giving more weight to supplier compliance in their sourcing decisions even when not compelled to do so by regulations (compared to 65% of businesses within the scope of ESG laws). Notably, sectors with a recent history of strong public scrutiny, such as Textile and Apparel, tend to have the highest percentage of businesses paying closer attention to supplier conduct.

As all stakeholders of global supply chains increasingly recognize the importance of ESG issues, this is a good time for brands to work with their suppliers toward greater transparency and sustainability. For established sourcing partnerships, this can mean revisiting the terms of cooperation to place a greater focus on human rights and environmental compliance; while buyers exploring opportunities in new sourcing markets should keep ESG concerns top of mind when choosing and onboarding new suppliers, to emphasize the importance of ethical and sustainable business from day one.

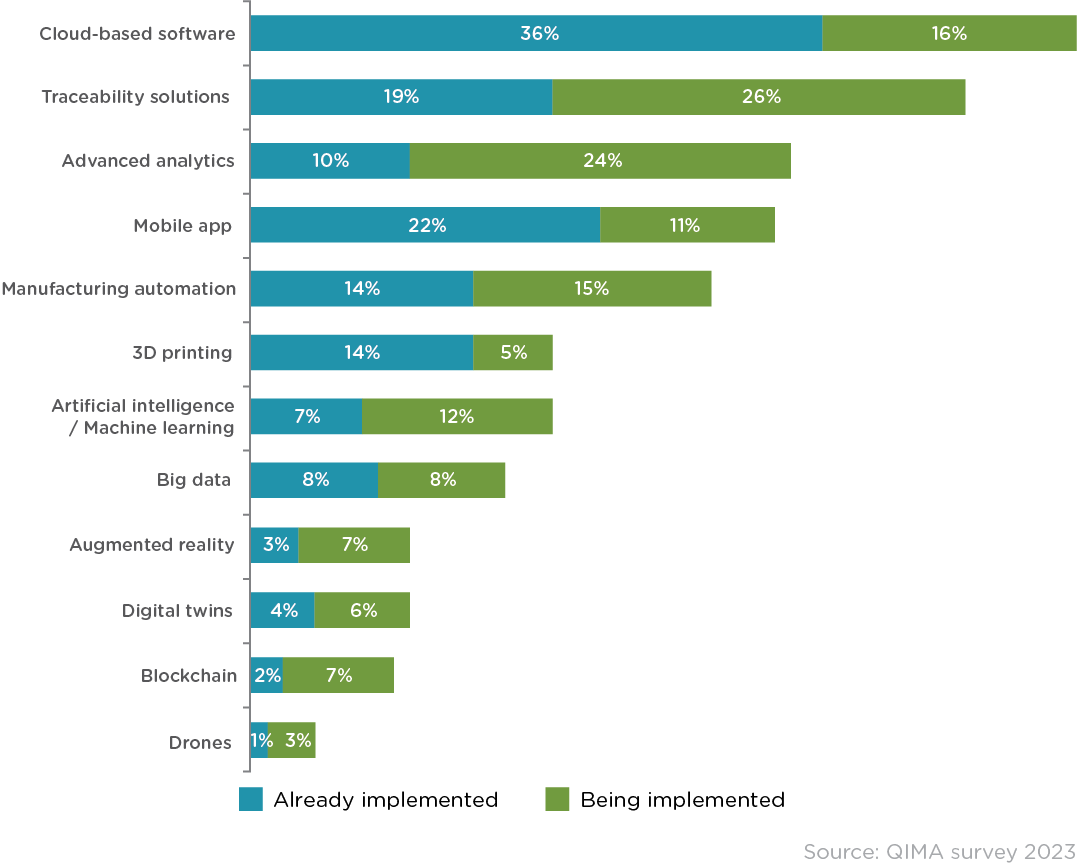

In QIMA’s H1 2023 survey, supply chain visibility was named as a top reason to invest in digitization, with traceability solutions being among the top three most popular supply chain technologies (already implemented and/or being implemented by 45% of respondents).

Fig. E1. “Does your business fall into the scope of any ESG legislation?” (by respondent HQ location)

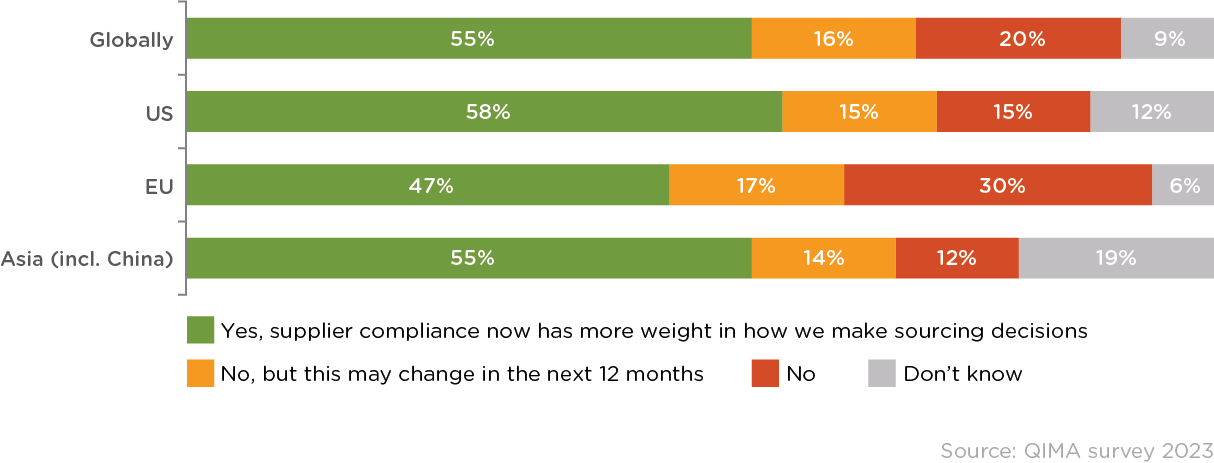

Fig. E2. “Does supplier compliance have a stronger impact on your sourcing decisions now compared to 12 months ago?” (by respondent HQ location, regardless of whether respondent is within scope of ESG legislation)

Fig. E3. “Which of the following technologies has your company already implemented / is planning to implement in your supply chain?”

China Remains Deeply Intertwined in the West’s Supply Chains

Following the first quarter’s promise of a comeback, China sourcing has remained on an upward trend throughout the first half of the year, albeit with a slow growth pace, QIMA data shows. Globally, demand for China inspections and audits was up +3.5% YoY in Q2 ‘23, behind China’s revised 2023 growth forecast of 5.6%.

As before, emerging regions proved the strongest drivers of this growth, with Q2 inspection and audit demand from businesses based in Latin America and Asia up +13% YoY and +27%YoY, respectively, compared to the flat demand from Western buyers in the same period.

Without underplaying the importance of the emerging regions’ domestic consumer markets, it is worth noting that many of the countries currently registering a strong uptick in China sourcing are also on the receiving end of new business volumes from global buyers that have been shifting their procurement away from China. This suggests that despite the long-term efforts of American and European brands to decrease their reliance on China, the manufacturing giant remains deeply intertwined in Western supply chains, being a key supplier of raw materials, components and intermediate products to other sourcing markets in Asia as well as the US’s nearshoring grounds in Mexico and other parts of Latin America.

Southeast Asia Sourcing Trends Positive, but Growth Varies from Country to Country

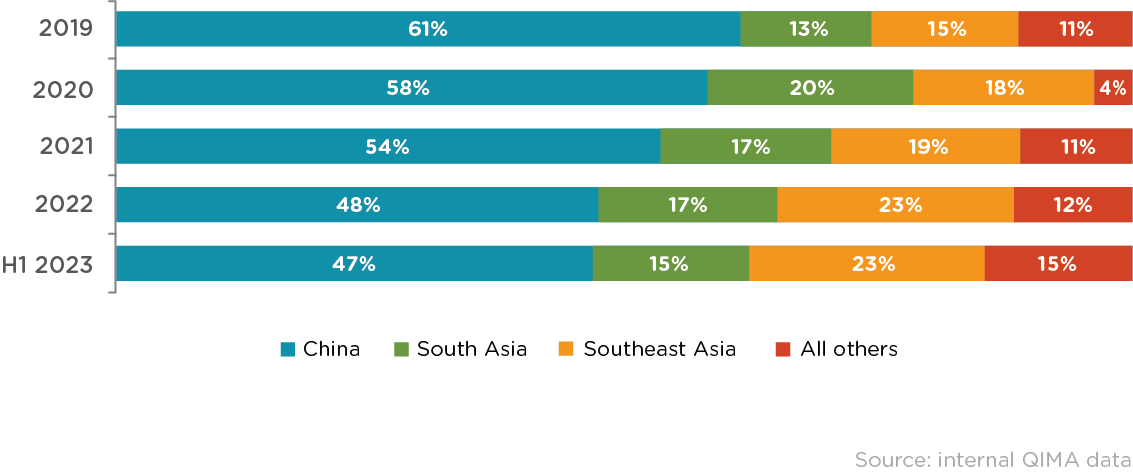

Meanwhile, 2023 is proving promising for Southeast Asia sourcing, with QIMA data showing a steady expansion of inspection and audit demand in the region, and sustained interest from Western buyers. The combined share of Southeast Asia’s sourcing markets in the buying portfolios of US- and EU-based brands has been steadily growing, and in H1 2023 amounted to almost half of that of China (compared to one-third in 2020).

Growth rates, however, vary throughout the region, with Vietnam sourcing experiencing a slower H1 2023 compared to some neighbors; contributing factors include the mounting bureaucratic hurdles linked to Vietnam’s ongoing anti-graft campaign, and a recent series of power outages. QIMA data on Vietnam inspection and audit demand in Q2 2023 shows a +6% YoY expansion globally, and a +5% YoY for US and EU buyers, compared to a faster growth shown by some other players in the region.

Fig. S1. US and EU buyers’ top sourcing markets by share

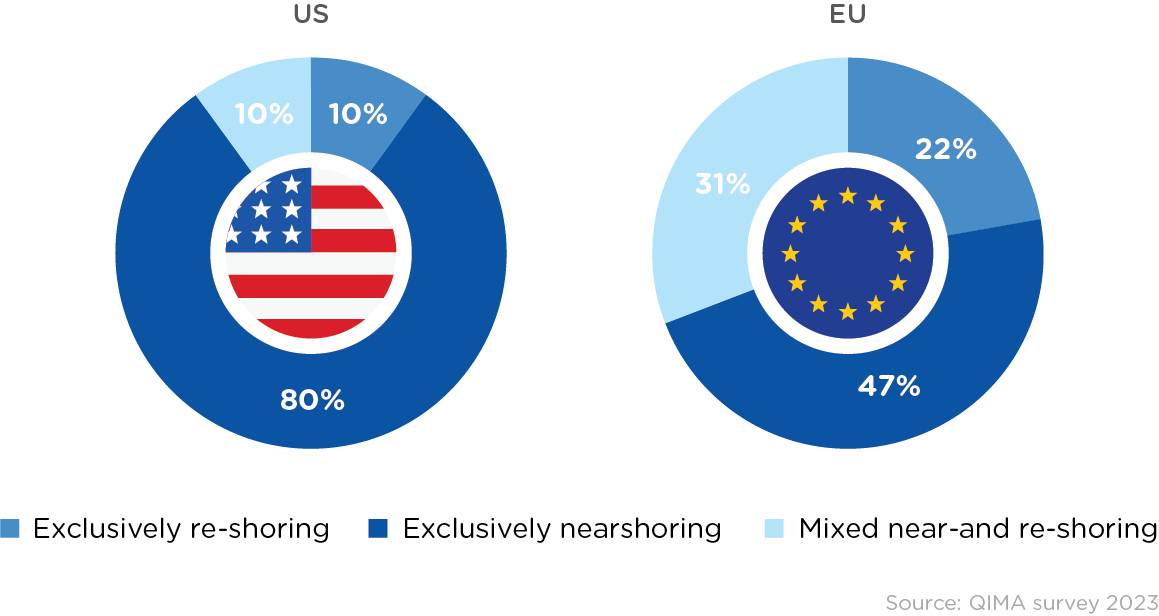

Nearshoring vs. Reshoring: EU Buyers Leverage both, while US Brands Prefer Sourcing from Neighbors

Brands worldwide continue to leverage nearshoring and reshoring as part of their procurement strategies, but European and American buyers take different approaches to bringing a portion of their operations closer to their respective consumer markets.

US buyers overwhelmingly prefer nearshoring over reshoring as an alternative to overseas sourcing, with only 20% reporting buying more from their home country in the past 12 months, QIMA’s H1 2023 survey shows. Meanwhile, EU-based businesses favor a more flexible approach, using a combination of home region sourcing and buying from the neighboring regions to shorten their supply chains. QIMA’s H1 2023 data on inspection and audit demand from EU-based buyers shows double-digit expansion in Central and Eastern European countries, as well as a steady uptick in Western European countries, including Italy, Germany, Portugal and Spain.

Among the drivers for European reshoring are the continued gradual disengagement from China due to geopolitical tensions and the ongoing push to increase the EU’s self-reliance for electronic components. In the meantime, European textile and apparel markets still rely strongly on suppliers in the Mediterranean and the Middle East: QIMA data shows inspection and audit demand from EU buyers in the region growing +22% YoY in Q2 2023.

Figure N1: “Have you started purchasing or increased your purchases from suppliers in your home country or region within the last 12 months?”

In the Dawning Age of Mandatory ESG, Supply Chain Transparency is the Way Forward

After the past few years’ steep learning curve, businesses with global supply chains have gotten better at navigating change – just in time to tackle the new challenges brought about by the tightening of ESG regulations. Now more than ever, end-to-end transparency and traceability are crucial for managing supply chain risks in a world where responsible sourcing is fast becoming non-optional.

Press Contact

Email: press@qima.com